Less Than Secure: The Insolvency Of The Social Security Trust Fund Is In Sight

June 24, 2026

When we last addressed some of the problems facing the Social Security Administration, those problems centered on the chaos and confusion caused by significant staff layoffs and budget cuts earlier in 2025 and 2026, as well as the looming threat of the Social Security Trust Fund running out of money sometime in the next decade. All of these issues are still present, and there’s an added sense of urgency, given the recent release of the 2026 report of the Social Security Trustees.

Let’s start with the current administration of the Social Security Administration (SSA). According to recent reporting in The New Yorker, with more than 7000 employees gone, including over 3000 who had direct contact with the public, the SSA is struggling to respond to requests and problems, and workers are overwhelmed in their efforts to provide access and benefits to the public. The administration suggests that technology upgrades and streamlining have produced a more organized and responsive agency. However, it appears that much of the work has been centralized far from the field offices where, formerly, the public could get answers and help with their SSA problems. One new effort the agency has begun is also important to flag: For anyone previously receiving a paper check for their Social Security, you should have received notice that the agency is now switching over completely to direct deposit, for reasons they describe as efficiency, reduction of costs, and enhancing security. Those who have previously received checks will now need to set up direct deposit into a bank account, or, if no bank account is available, onto a debit card. For more information about this changeover, click here. For those who have tried unsuccessfully to get help with Social Security problems from the SSA, you may want to check out the suggestions of non-governmental sources of help here.

But more than ever, Social Security recipients and those close to claiming Social Security are dependent on these benefits and are relying on their continued payment. In a recent poll cited on the website 24/7 Wall Street, 56% of Social Security recipients stated that they could not even afford to miss ½ of one of their monthly payments, and an overwhelming majority are worried that Social Security may run out of funding sometime during their retirement. That data just underscores how little financial cushion a significant portion of our senior population has and how reliant so many are on their monthly payments. It’s estimated that Social Security covers, on average, 59% of a recipient’s retirement expenses and that many recipients, due to inflation and high costs, are now not only cutting back on discretionary spending but on essential spending, such as food and medication. Many are closely watching what will happen this October, when the new COLA (Cost of Living Adjustment) is made for 2027 payments. Right now, due to inflation, recipients are hoping for a big boost in the 2027 COLA, which, during COVID, went up 5.9% in 2022 and 8.7% in 2023. Current estimates are that the 2027 COLA increase might be up to 3.8%, at least according to the Senior Citizens’ League, which has a COLA Watch column. Other sources estimate that the jump could be as high as 4.7%.

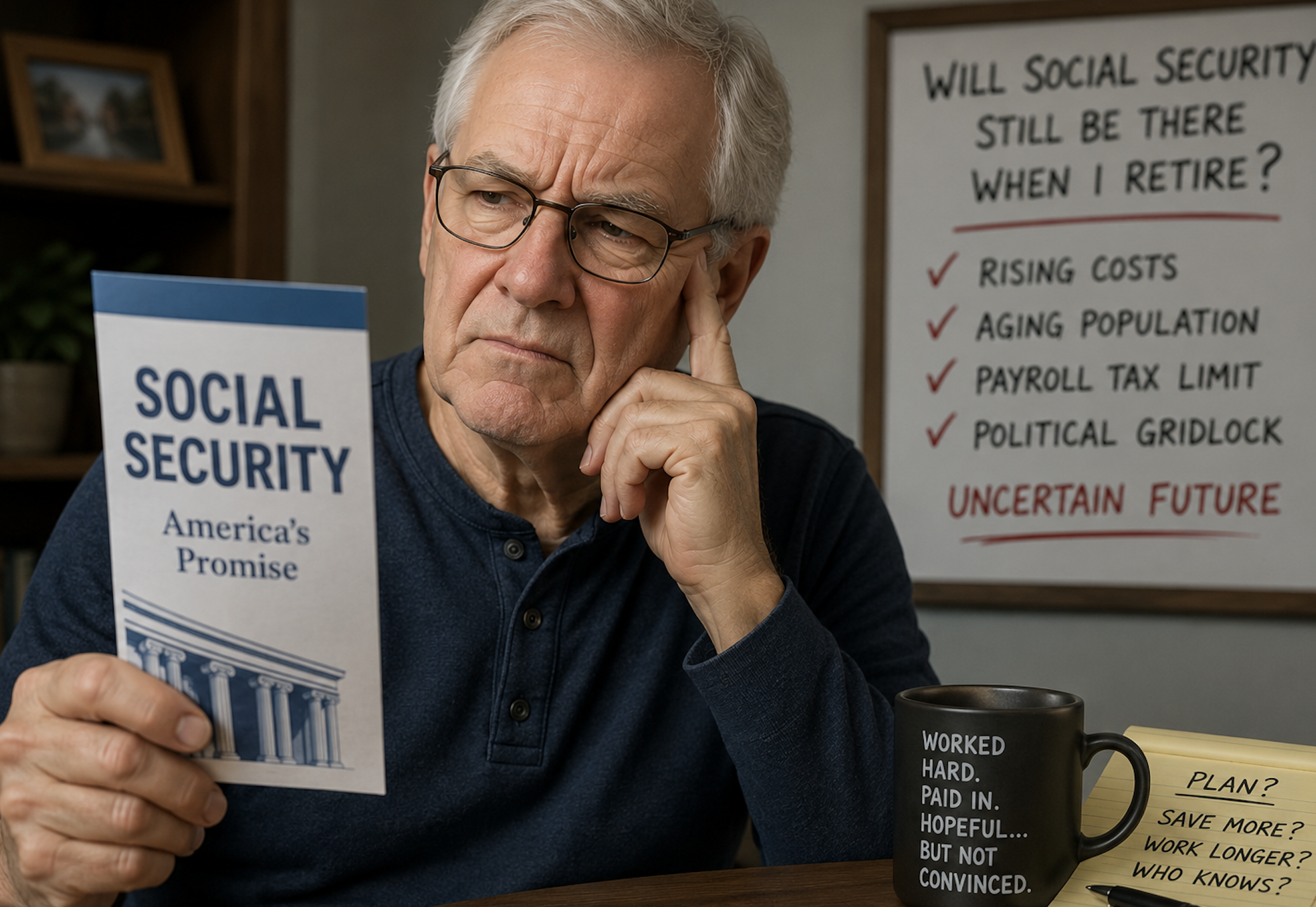

Perhaps more than ever, however, all eyes are on the latest Social Security Trustees Report, which estimates that the Social Security Trust Fund, which makes up the gap between benefits owed to recipients and revenue coming into Social Security, will run out of money by the end of 2032, which is just 6 years away. That’s a revised estimate from last year, when it was expected to run out in 2033. Why is there such a shortfall, and what has caused its acceleration? There is a confluence of problems contributing to the shortfall, including declining birth rates, less immigration (meaning fewer workers contributing to the system), increasing retirement among baby boomers, less revenue due to significant federal tax cuts, and older adults living longer. What that shortfall means is the following: Social Security will be able to continue to pay out benefits, but they will be reduced in amount, as the incoming revenue is expected to only cover 78% of payments owed. That means Social Security recipients could see their benefits cut by up to 22% each month.

While there is always the option for Congress to borrow more money, the reality of the exploding federal deficit and elevated interest rates means that option is likely not available or desirable. Nonetheless, this will be something that Congress must begin to deal with, as whatever fix is developed will require new federal legislation passed by Congress. In fact, those running to be elected to the Senate this fall will be in Congress to deal with this issue, and should face questions from voters as to how they propose to fix Social Security to avoid benefit cuts.

So what proposals might be on the table for fixing this funding gap for Social Security? Numerous proposals are floating around, including some raised in a citizens’ guide put out over a decade ago. Most experts and policy watchers agree that there will either need to be benefit cuts, revenue increases, or some combination of those. However, each has its own political constituency along with adversaries, and like everything in politics, there will need to be bargaining, negotiation, and compromise. When it comes to raising revenues, Senators Bernie Moreno and Elizabeth Warren have just put forth a bipartisan proposal to eliminate the payroll cap on income taxed for Social Security. The current cap is taxing income up to $184,500, which is more than most people earn, which means most people pay Social Security taxes on their entire income. These Senators propose that the only fair system is for everyone to pay Social Security taxes on all of their earned income, a position they say the majority of Americans, regardless of party, support. Others have proposed raising the cap rather than eliminating it, or even taxing all income, including investment earnings. Some recent surveys have also suggested increasing taxes for younger workers to bolster the Trust Fund.

Proposals to cut benefits include placing a cap on how much Social Security a couple can receive (suggestions are to cap the benefits at $100,000 per couple) or to place a cap on the yearly COLA increase, perhaps targeting those who receive the highest level of benefit. There have also been suggestions to raise the retirement age beyond its current age of 67, though that could penalize low-income workers who may have more physically demanding work that would make later retirement more difficult.

Likely, some combination of these measures will be enacted, though given the glacial pace at which Congress acts these days, there are likely to be many dramas and anxieties raised before a solution is developed. No doubt there will be winners and losers in this process. Let’s just hope it’s transparent and considered, as millions of Americans have a stake in these deliberations.