House Poor: Older Adults Increasingly Cannot Afford A Home

March 18, 2026

There is the sense in the mainstream media and popular culture that Baby Boomers have it made: They own their own homes in significant numbers, have paid off mortgages, and will reap a huge financial reward when they decide to sell and downsize. And to some extent, for some of us, that is true. Close to 79% of older adults own their own home, and after decades of paying down a mortgage, a significant number of older homeowners are mortgage-free at this point. However, that is not the end of the costs of home ownership, as most of us likely know. Between home insurance, property taxes, utilities bills, and maintenance costs, it’s not cheap to own a home, even if you no longer have a mortgage, and for many older adults, rising costs are putting pressure on their ability to stay and maintain their homes (and pay for safety and design changes that allow for aging in place). Additionally, a nationwide housing shortage and high interest rates are making it challenging to contemplate downsizing to a smaller, less expensive home. And for those who do decide to sell their homes, new data from the Center For Retirement Research reports that, on average, older sellers receive a lower return on their home sales than younger sellers, either because their house is in disrepair or they are not taking advantage of the competitive market found on a multiple-listing service. Beginning at age 70, the gap widens between what an older seller receives for a house sale and what a younger seller would receive for a comparable house. Older homeowners may have put off routine maintenance or more modern upgrades, so that, on average, they are receiving about 5% less than a younger seller would. Bottom line? Timing your house for a late-in-life sale may come at a financial cost.

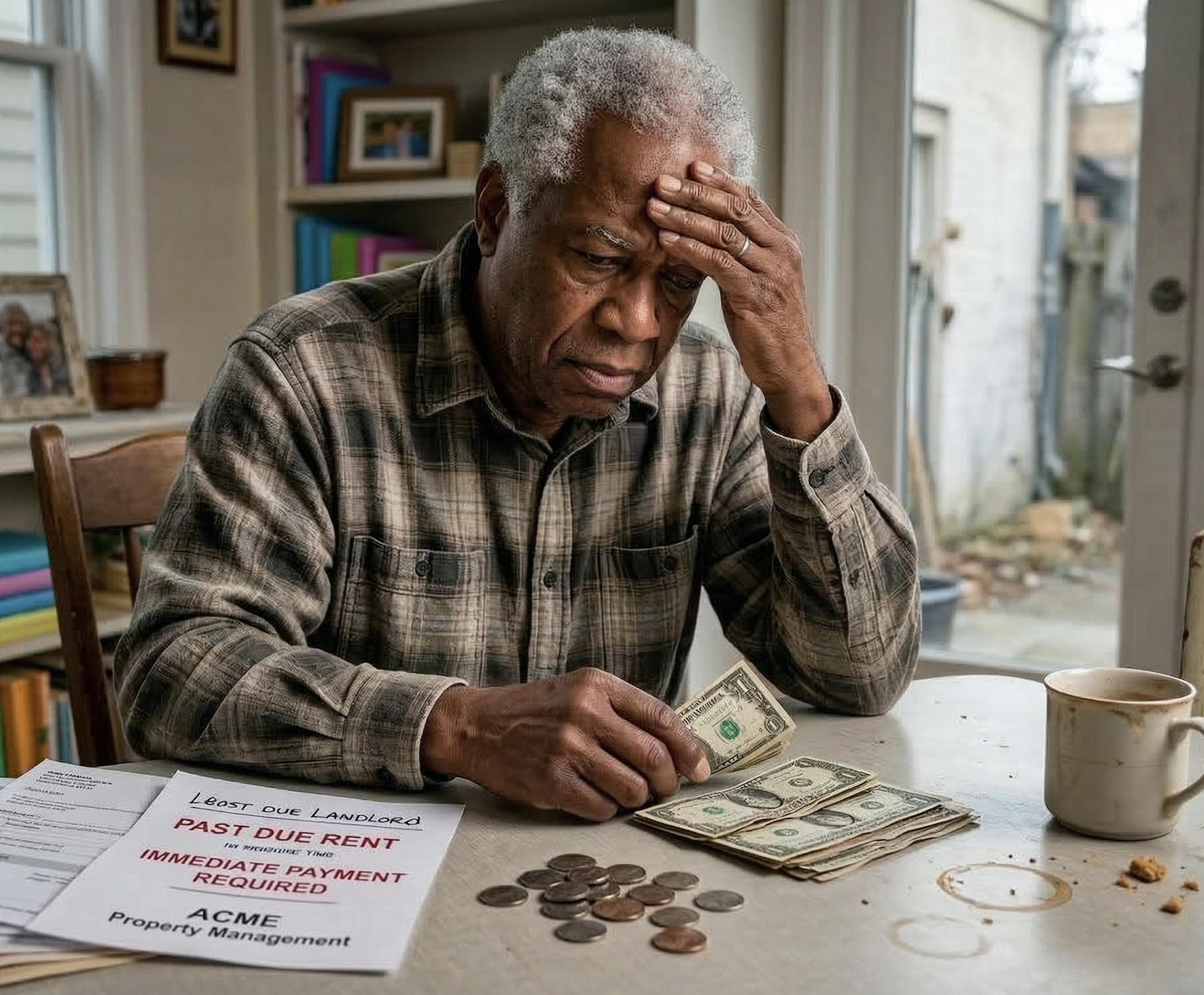

But there’s another worrisome trend when it comes to housing and older adults: The rise in older renters, leaving older adults vulnerable to unexpected and unaffordable rent increases. According to data from 2024, the average retiree spends about $1849 per month on housing costs: rent/mortgage/taxes/utilities/maintenance/other household expenses. It’s the largest expenditure each month for most older adults, and those costs can quickly escalate and become difficult to sustain in a competitive rental market where rents may be rising each year, above and beyond the fixed incomes of most older adults. In fact, according to US Census Data, between the years 2013 and 2023, the number of older renters (aged 65 and older) increased by nearly 30%. It was the largest increase in renters of any age group. The increase may be due to a number of factors, including the need to downsize, the unaffordability of purchasing a new home due to high interest rates, and a desire to relocate to be closer to family. In essence, as the population ages, more and more of us are becoming non-owners while competing for affordable housing that meets the needs of older adults.

The challenge is how those living on a fixed income handle ever-increasing prices, along with the other housing costs incurred, even if you rent rather than own. A recent report from the Joint Center for Housing Studies at Harvard found that one in three older adult households is “cost-burdened” with housing costs, meaning that they pay more than 30% of their monthly income for their housing, and more than 50% of those “cost-burdened” are actually “severely” cost-burdened, because they pay more than 50% of their monthly income on housing. The numbers are staggering: 58% of older renters were considered cost-burdened in 2023, with the majority actually being severely cost-burdened. If you factor in other essential costs, such as food, medical care, and transportation costs, you can see how this quickly becomes unsustainable for a large percentage of older adults. As the Urban Institute recently summed it up, “America’s housing market is failing older adults.” Moreover, the expensive and limited housing stock available for older adults is also triggering a new wave of homelessness among seniors. According to the Urban Institute report, between 2019 and 2022, the share of older adults who were homeless increased by 37%. In 2025, one out of every five people who were homeless was aged 55 or older. Given the rising prices in every aspect of life, it’s not hard to imagine that one tragedy- an illness, an accident, a job loss, the death of a spouse- could send anyone into a state of homelessness or housing insecurity. That’s the situation for 67-year-old David Bourassa, recently profiled in The Boston Globe, who lost his home of 20 years following a cancer diagnosis and is now struggling to survive a huge rental increase in a housing development formerly limited to low-income seniors but now moving to market rental rates. For many of us, it’s easy to imagine a similar scenario sending us into a tailspin. And while the Federal Department of Housing and Urban Development does have financial aid programs for low-income seniors, it’s not clear how many will survive or in what form, given Federal budget and programmatic cuts.

So, while some older adults seem to have it made in terms of housing and stability, a significant number are one tragedy away from struggling to keep a roof over their heads. It feels scandalous that in a country this wealthy, older individuals should be put in such a position.