By Kathleen M. Rehl, Ph.D., CFP®, CeFT® Emeritus

The death of a spouse is not only heartbreaking. It can also thrust a woman into a maze of decisions she may not have expected to face alone. In the midst of grief, even routine money matters can feel unfamiliar. And often, the hardest part is not the obvious bills or paperwork. It is the financial surprises that show up quietly, weeks or months later.

Although I’m writing about widows in this article, many of these same financial surprises can affect widowers as well.

Here are three that many widows do not see coming, along with practical ways to prepare for them or respond with confidence.

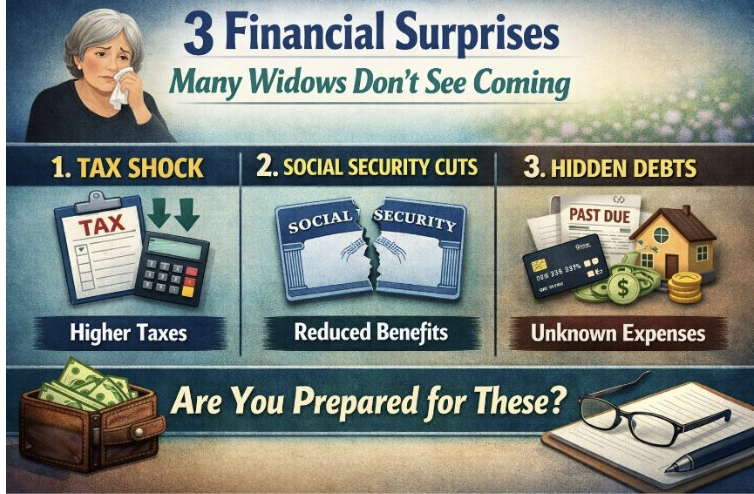

The tax hit can arrive sooner than expected

One of the biggest surprises for many widows is that taxes may go up even when household income goes down. A couple may file jointly in the year of death. After that, the surviving spouse may need to file as single or, in some cases, as a qualifying surviving spouse for a limited time if she meets the rules. That change can affect deductions, tax brackets, Medicare premiums tied to income, and the taxation of retirement account withdrawals. The IRS notes that “qualifying surviving spouse” status is available only for two years following the year of death if eligibility rules are met.

Example:

Linda’s husband handled the taxes for years. After he died, she continued taking the same IRA withdrawals they had always taken together. But when she later filed on her own, she learned her tax picture had changed. She was no longer benefiting from the same filing structure, and the withdrawals pushed her into a less comfortable tax situation.

Helpful steps:

A good tax review after widowhood is not a luxury. It is often a form of protection.

Social Security may not work the way you assumed

Many widows think they will continue to receive the same Social Security income the household had before. Unfortunately, that is usually not how it works. When one spouse dies, one check stops. A widow may be eligible for survivor benefits, but the amount depends on her age and the timing of her claim. The Social Security Administration says surviving spouses can receive a reduced benefit starting at age 60, and up to 100% of the deceased spouse’s benefit if they claim at full retirement age for survivor benefits. (Social Security)

This catches many women off guard because household expenses do not instantly drop by half when one person dies.

Example:

Maria and her husband had relied on two Social Security checks to cover monthly basics. After his death, she learned she could not continue receiving both benefits in full. She had to decide whether to claim survivor benefits right away at a reduced amount or wait for a larger monthly payment later.

Helpful steps:

This is one area where timing matters. A thoughtful claiming decision can affect your income for the rest of your life.

Hidden debts and household costs can surface after the funeral

Another painful surprise is discovering debts, subscriptions, bills, or home expenses a widow did not know existed. Some women learn that their spouse had a credit card balance, a personal loan, or a business obligation. Others find that the real issue is not debt itself, but the ongoing cost of maintaining a home alone: insurance, repairs, property taxes, utilities, and help with tasks a spouse used to handle.

The Consumer Financial Protection Bureau explains that a deceased person’s debts are generally paid from the estate, and a surviving spouse is usually not personally responsible unless the debt was shared, co-signed, or responsibility applies under state law. (Consumer Financial Protection Bureau)

Example:

Sharon thought her finances were simple. Then she found an old home equity line, two auto-pay subscriptions, and a rising home insurance bill. None of it was catastrophic on its own, but together it changed her monthly cash flow more than she expected.

Helpful steps:

Often, what feels like “I’m bad with money” is really “I’m seeing the full picture for the first time.”

A gentle closing thought

Widowhood brings enough emotional weight without financial confusion piled on top. If any of these surprises sound familiar, please know this: you are not behind, and you are not alone. Many capable women discover these issues only after loss.

A steady next step is to sit down with a trusted financial planner, tax professional, attorney, or Social Security rep who can help you sort through the details with care.

Call to action:

If you are widowed—or helping someone who is—choose one simple money step this week: review Social Security, gather account statements, or schedule a conversation with a trusted professional. One small step today can create more clarity for tomorrow.

Kathleen M. Rehl, Ph.D., CFP®, CeFT® Emeritus, authored the award-winning book Moving Forward on Your Own: A Financial Guidebook for Widows. She received the 2025 Excellence in Research Award for Adjunct Faculty from The American College of Financial Services. Kathleen owned Rehl Financial Advisors for nearly two decades before launching her encore career—empowering widows through her writing, speaking, research, and mentoring. Now “reFired,” Kathleen continues to do work she finds fulfilling. Her writing has appeared in The New York Times, The Wall Street Journal, agebuzz, CNBC, Nerd’s Eye View, Rethinking65, and other notable publications. She is also an INELDA-trained end-of-life doula. Free resources are available at KathleenRehl.com.

![]()

Sign up for agebuzz’s free weekly newsletter sent every Thursday